Card Scheme rules and fees: What are they?

Card schemes, like Visa and Mastercard, regularly update their rules and fees. It can be hard to keep up, but if you’re with a payment provider, like Total Processing, then we will help keep you in the loop so that you don’t pay more than you need to.

In this blog, we’ll cover the rules around declined transactions for both in-store and online payments and how the merchant should handle them.

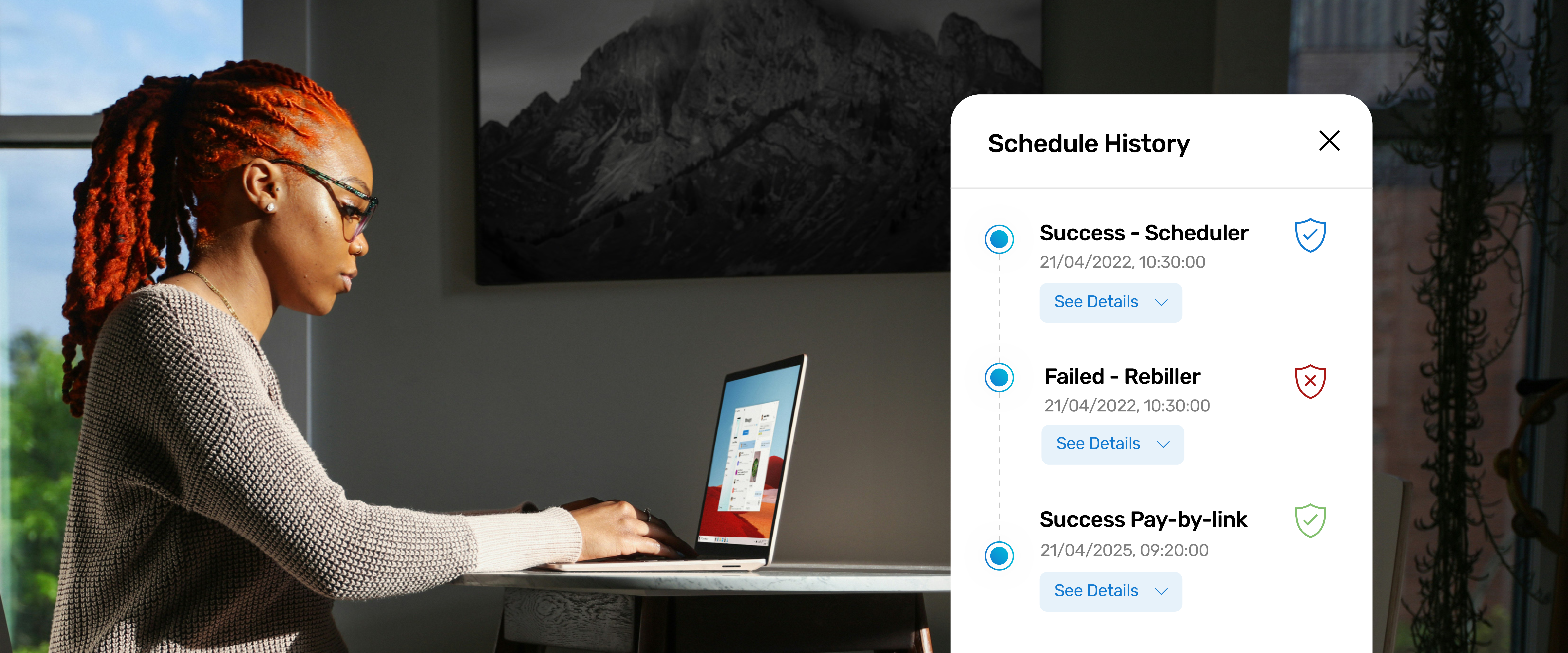

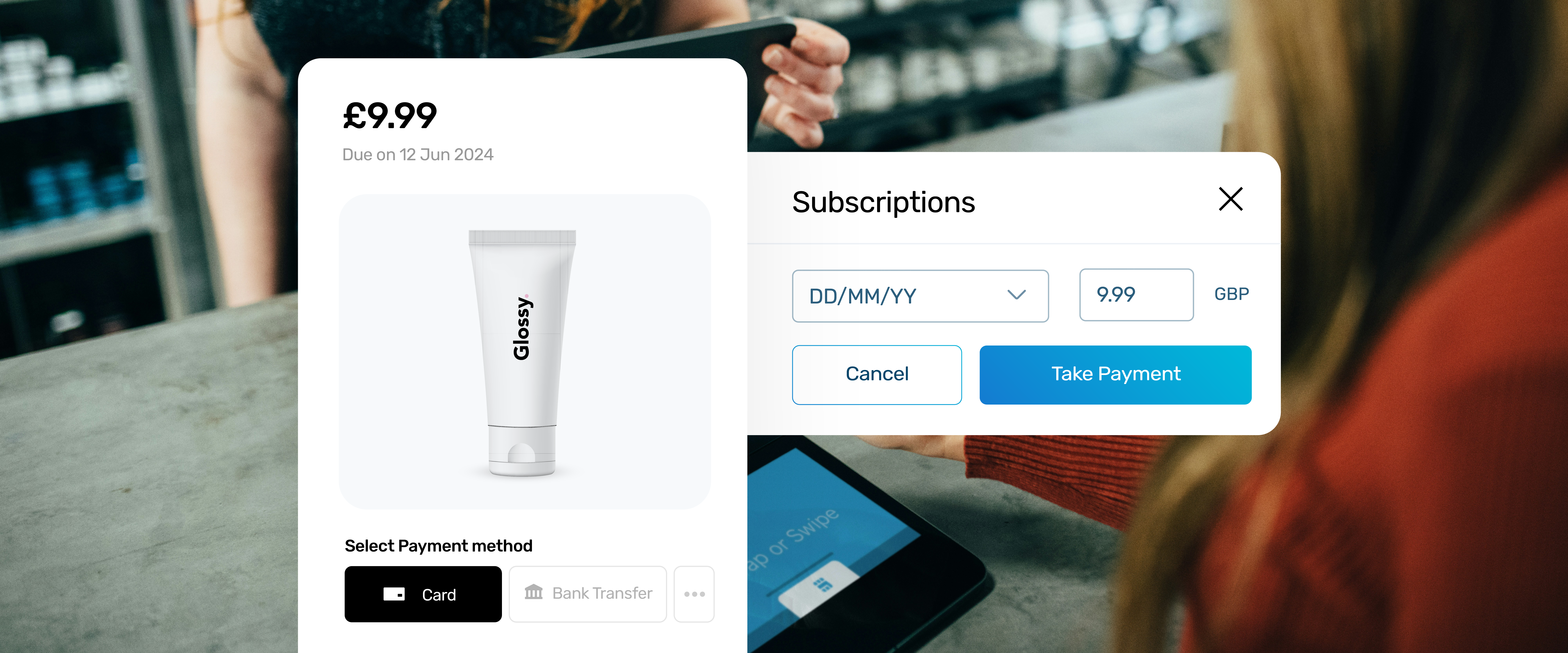

The card schemes have a set of Merchant Advice Codes (MAC). If you haven’t heard of them, they are reasons why a transaction has been declined which the issuer will send to the merchant. Depending on which MAC is sent will decipher whether the transaction can be reattempted or not. If you’re advised not to reattempt it and you ignore this advice then, you, the merchant, will be charged a fee.

You may be wondering why there are more potential fees on top of the usual issuer fee (a small charge from the card schemes to use the network or software that the card operates on), but the card schemes set rules to improve the payments ecosystem. The goal is to increase transparency when an authorisation is declined and reduce unnecessary reattempted transactions. The only way to enforce this rule is to charge a fee for those who don’t comply.

The descriptive response codes make it much easier for issuers to identify why they are declining the transaction allowing acquirers and merchants to correct the issues and determine how or whether they should reattempt the transaction. Adopting these authorisation best practices can help to improve approval rates, so it’s worthwhile for more than just avoiding the fee.

There is a range of Merchant Advice Codes, and they will differ depending on the card scheme. They can range from expected fraudulent activity to an expired card, to the customer not having enough funds in their account.

A few of the most common MACs include:

And the list goes on, but the issuer themselves will best advise you on the specific codes.

The best way to avoid the fees is simply to follow the rules. Declined transactions aren’t ideal for anyone involved; the cardholder, issuer, acquirer and merchant, but to continue to reattempt the transaction will only cost the merchant more fees and cause more embarrassment and inconvenience for the cardholder.

The response codes are made clear for a reason so that there should be no confusion as to whether you should try again or not.

Hopefully, you’ll now have a better understanding of what the Merchant Advice Codes are and why they’re important. But if you want some more information, feel free to reach out.