Find The Right Partner. It Pays.

Same Day

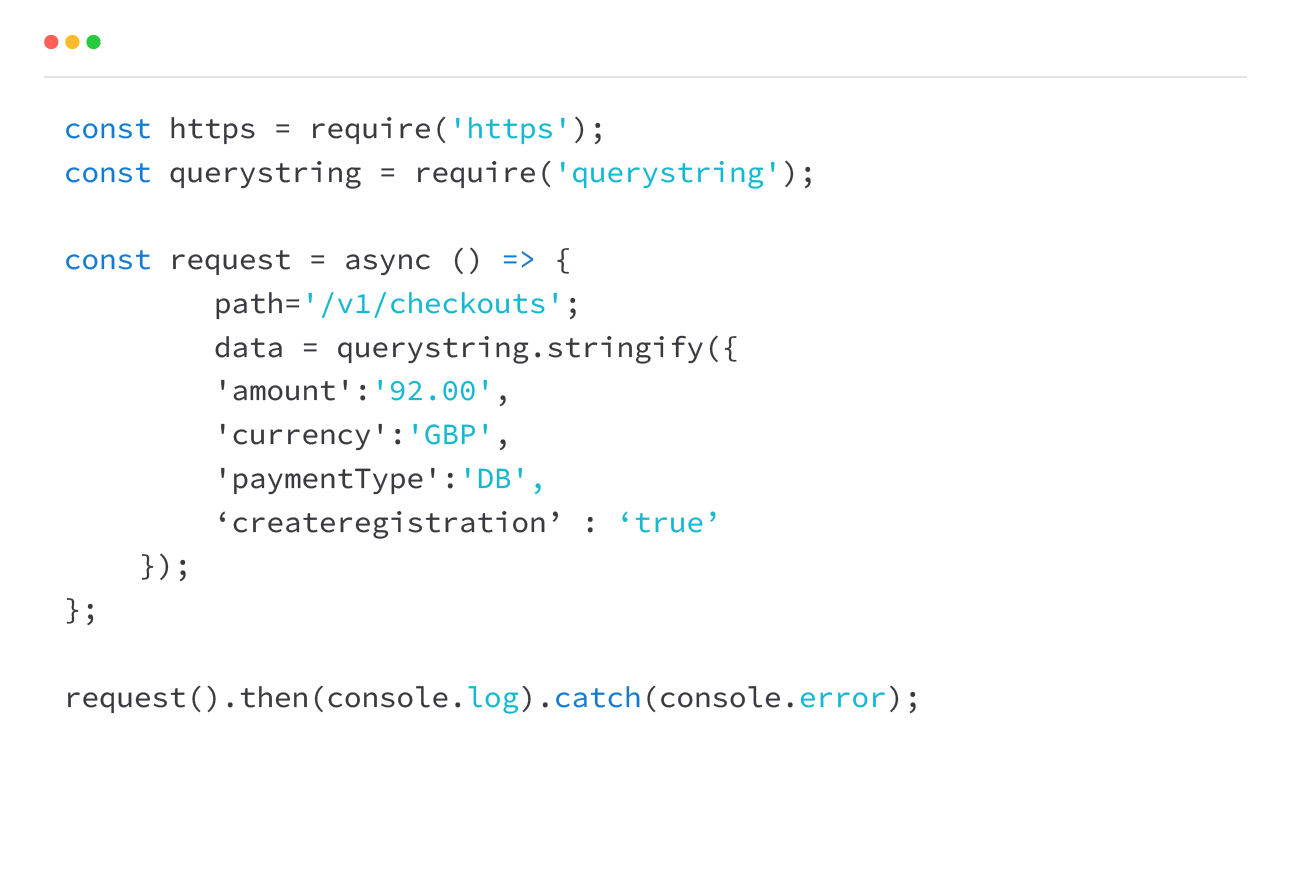

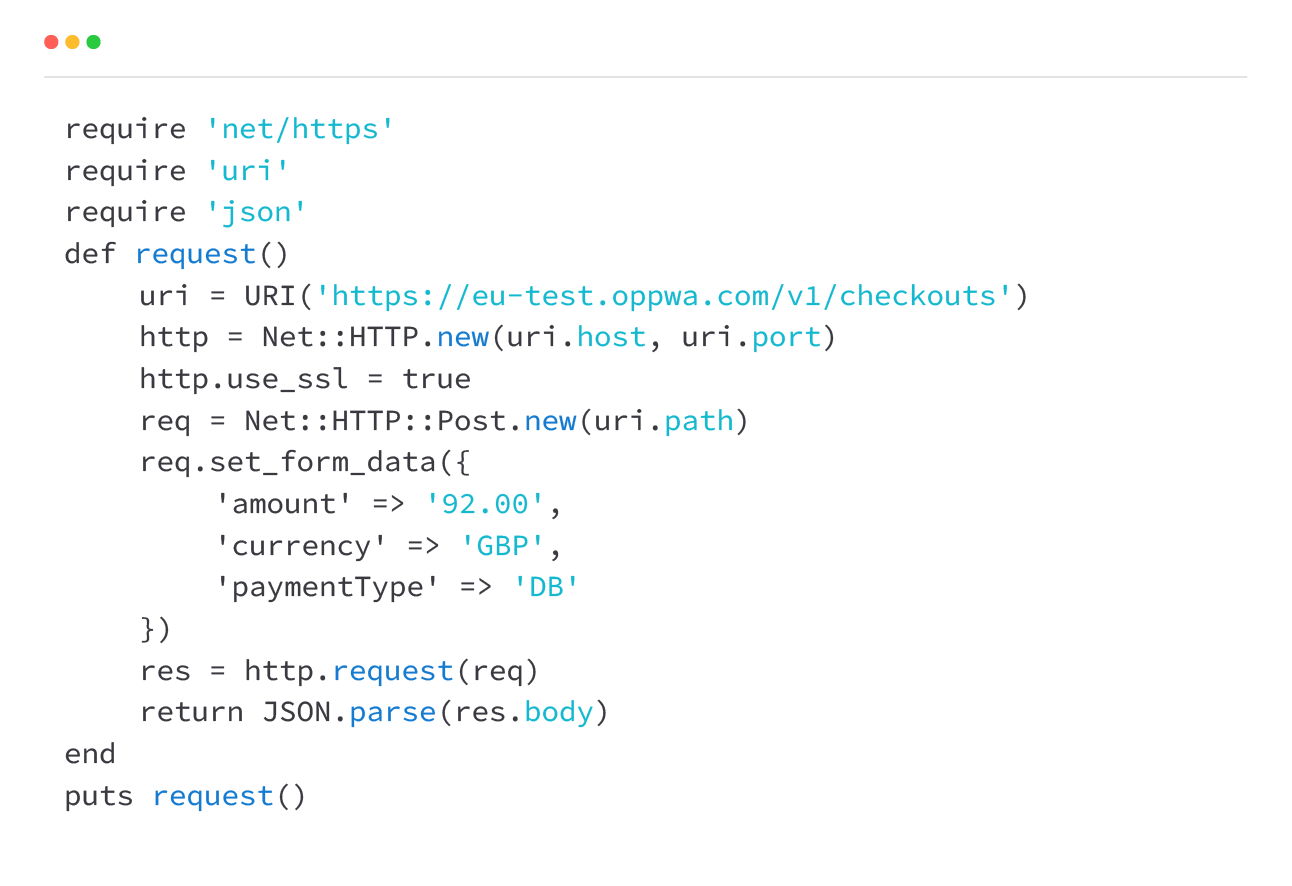

Integration

Same day integration into your platform of choice, assisted by our in-house developers and payment specialists.

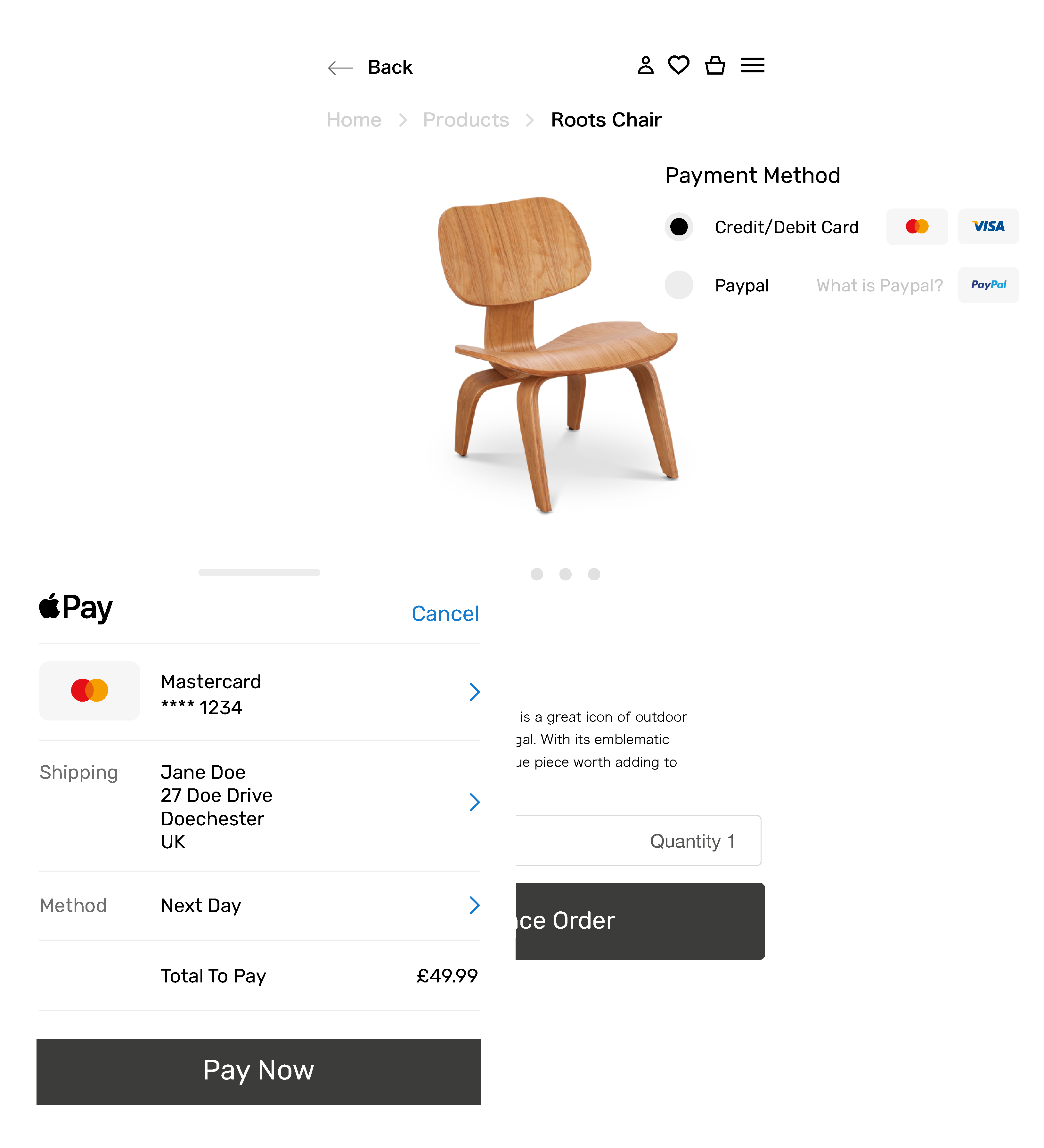

Alternative

Payment Methods

Discover more avenues to higher revenue, with more than 198 payment methods available worldwide.

Fraud & Risk

Management

Our payment gateway solution comes complete with a variety of fraud and risk tools to protect your business.

180

Currencies

Take payments from global customers — with more than 180 presentment currencies available at the checkout.

Our Solutions

Our expert team will help you avoid complex and unnecessary issues when taking payments. We make processing payments as seamless and secure as possible.

Easy Integration

Cost-Effective

Global Coverage

Seamless Integration – For Any Use

Discover a wide range of popular developer documentation for e-commerce interfaces including WordPress, Magento and Shopify.

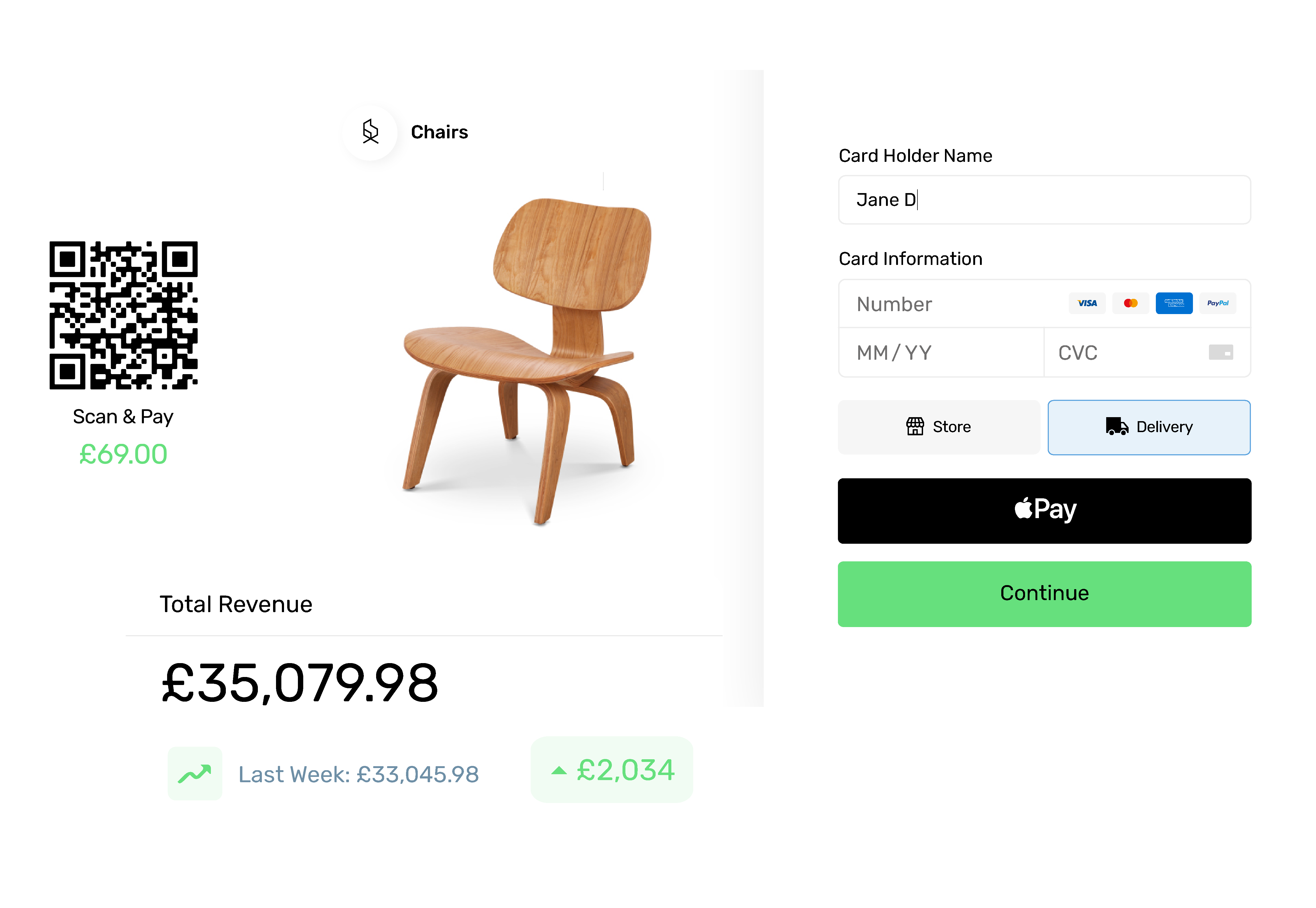

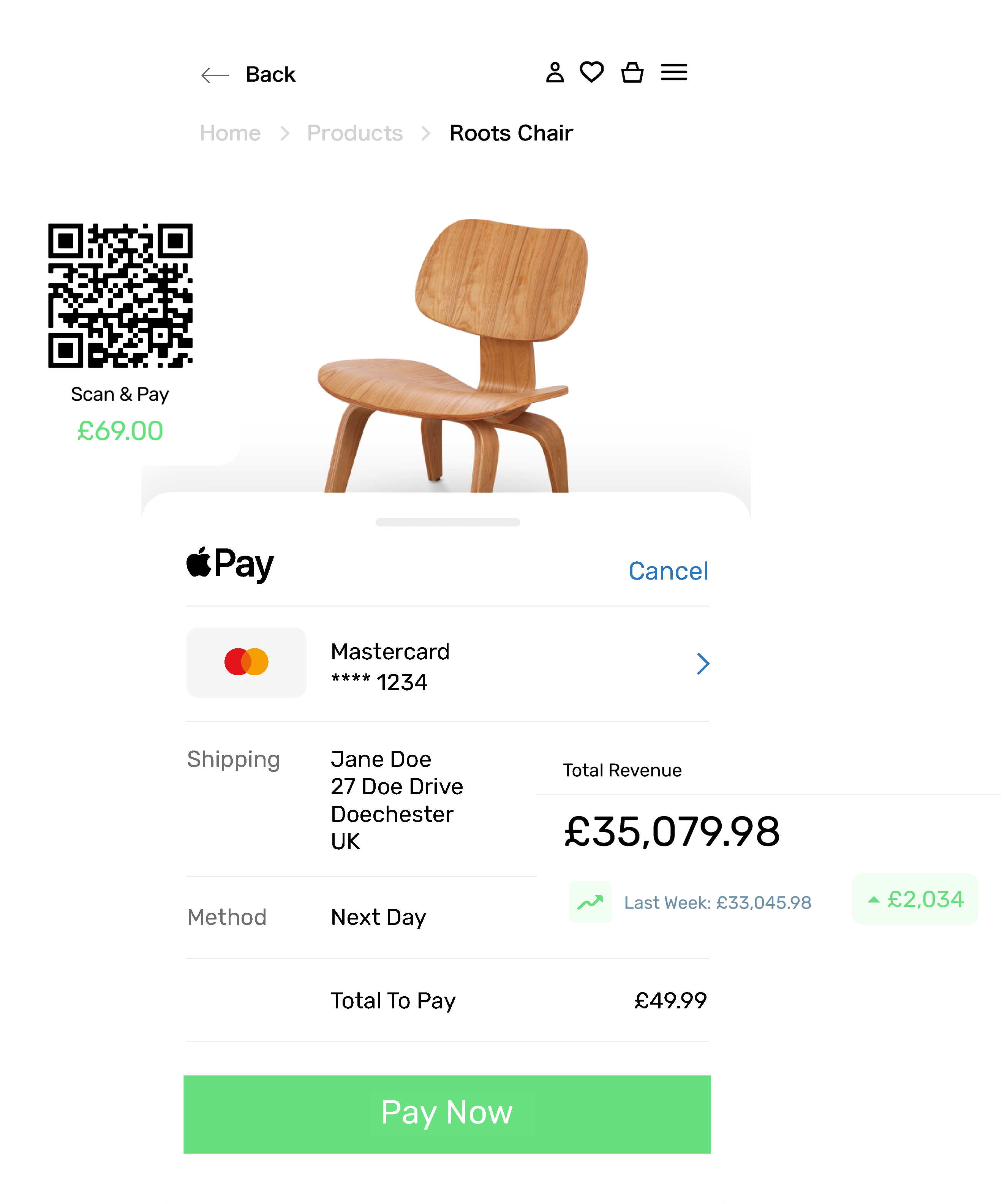

Start accepting popular payment methods including Apple Pay, Amazon Pay, Visa and American Express.

Ready To Start Accepting Payments?

Total Control is the all-in-one solution for your business.

Get a quote or schedule a call to demo our powerful suite

of features.

Payments Made Real

Our mission is to be the most customer-focused payments company in the world.

Efficient & Strategic

Uzo and the team at Total Processing worked around the clock to ensure we could scale our business quickly in a time of increasing demand. They were efficient and strategic in their solution, providing us with a solution we could effectively unify across all of our payment channels.

Matt Ball, Head of Strategy & Partnerships at Cignpost